per tgl 17 September 2013:

Volatilitas SUN Meningkat

Maftuh Ihsan - Selasa, 17 September 2013, 22:35 WIB

Bisnis.com, JAKARTA -- Semakin melebarnya kisaran imbal hasil yang masuk pada lelang sukuk, Selasa (17/9/2013), jika dibandingkan lelang sukuk pada dua pekan sebelumnya mengindikasikan meningkatnya volatilitas di pasar obligasi negara.

“Contohnya seri PBS005 sekarang imbal hasilnya di 9,125% - 11,5%, padahal pada lelang sukuk sebelumnya 9,325% - 11,5%,” tutur Fakhrul Aufa, analis obligasi PT Penilai Harga Efek Indonesia, Selasa (17/9/2013).

Direktorat Jenderal Pengelolaan Utang (DJPU) Kementerian Keuangan melaporkan nilai penawaran masuk ke lelang sukuk, Selasa (17/9), hanya mencapai Rp6,49 triliun, turun 30,2% dari Rp9,3 triliun pada lelang sebelumnya.

Adapun, nominal yang dimenangkan dalam lelang sukuk tersebut Rp1,1 triliun dengan rincian seri SPN Rp748 miliar, PBS005 Rp199 miliar, dan PBS006 Rp153 miliar.

Kendati terdapat penurunan penawaran masuk, Fakhrul menilai minat investor terhadap obligasi negara masih besar kendati pasar masih dibayang-bayangi ketidakpastian rencana pengurangan stimulus the Fed.

Saat ini, lanjutnya, pemerintah lebih selektif untuk menyerap penawaran masuk mengingat dana yang berhasil diserap dari lelang obligasi pada kuartal III/2013 sudah mencapai 90% dari target yang ditetapkan. (ra)

Editor : Rustam Agus

per tgl 16 September 2013:

Bond Issuance in Asia Surges Ahead of Fed Meeting

Companies and governments returned to Asia's bond markets in earnest this week, raising funds amid a recovery in emerging-market assets and ahead of next week's highly anticipated meeting of the U.S. Federal Reserve.

A total of $5.6 billion of bonds denominated in U.S. dollars, euros and yen were issued in Asia, excluding Japan, this week, according to data provider Dealogic. That's the most since the week ending May 13—the week before Fed Chairman Ben Bernanke first hinted that the central bank may begin to wind down its unprecedented monetary stimulus later in the year—a signal that sent borrowing costs sharply higher and investors fleeing from emerging markets.

Issuance in the past two weeks has totaled $9 billion, roughly the same amount issued over the previous nine weeks combined.

The rebound comes as many emerging-market financial assets—bonds, stocks and currencies—have rebounded following heavy selloffs in recent weeks. Indonesia's dollar bonds, for example, fell 20% between May and August but have risen 2.6% this month, according to HSBC. In all, dollar bonds in Asia have rebounded by 0.5% over last two weeks after tumbling by 7% during the past four months, according to the HSBC Asia Dollar Bond Index.

The rebound in Asian bonds is largely the result of greater stability in U.S. Treasurys after weaker employment data changed expectations about how quickly the Fed would wind down its stimulus, while reduced tensions over Syria improved overall sentiment, said Jon Pratt, head of Asia debt capital markets at Barclays PLC.

The market's return to a healthy level of activity also follows a colossal bond deal in the U.S.—

Verizon Communications Inc.'s

VZ +1.22% record $49 billion offering. It attracted orders of around $100 billion and resulted in frenetic trading as investors unable to get a piece of the initial offering snapped them up in the secondary market.

To be sure, investors remain selective about new bonds, and Asia remains on pace to record its worst quarter for bond issuance since the fourth quarter of 2011. Only $18.2 billion of bonds have been issued in Asia excluding Japan so far this quarter, less than half of the $44.1 billion in the previous quarter, according to Dealogic.

"Most of the Asian issuers these past two weeks were high-grade, government or government-linked borrowers that had planned to access the markets for some time and were waiting for the right window of opportunity," Mr. Pratt said.

That was the case for the Export-Import Bank of Korea, which priced a $1 billion dollar deal overnight Thursday. Hee-sung Yoon, head of the bank's international finance department, said strong demand for Verizon's offering, as well as those from the Russian and South African governments, convinced the bank that the timing was right.

Given that next week's Fed meeting could cause market volatility and there are also public holidays in South Korea, "we figured we couldn't pass the window," he said.

Borrowers have also paid more for their funds. Consider the $1.5 billion Islamic bond issued by the Indonesian government this week. The 5.5-year, dollar bond carried a yield of 6.125%, well above the 3.3% interest rate on a $1 billion, 10-year Islamic bond sold in November last year. A longer duration would usually draw a higher interest rate, all other conditions being equal.

Bankers are hopeful that more new bonds will be issued should markets remain stable after next week's meeting of the Fed. A majority of economists surveyed by The Wall Street Journal recently said they expect the Fed to say after next week's policy meeting that it will begin withdrawing its stimulus.

"Substantial caution remains," said Duncan Phillips, head of Asia-Pacific Debt Syndicate at Citigroup Inc. "But it has been shown that short periods of stability combined with pragmatic borrowers can produce great results."

RABU, 11 SEPTEMBER 2013 | 12:09 WIB

Investor Percaya Indonesia Aman 11 Tahun ke Depan

Investor Percaya Indonesia Aman 11 Tahun ke Depan

TEMPO.CO, Jakarta - Menteri Keuangan Muhammad Chatib Basri mengapresiasi lelang Surat Utang Negara yang digelar Selasa kemarin, 10 September 2013, dan berhasil meraup Rp 12 triliun dari total penawaran Rp 32 triliun. Menurut dia, sebagian besar membeli surat utang yang tenornya 11 tahun. "Artinya, investor lihat Indonesia 11 tahun ke depan masih aman," kata Chatib di kantor Presiden, Selasa malam, 10 September 2013.

Meskipun apresiasi dari investor cukup bagus, Chatib tak mau terburu-buru menyimpulkan bahwa situasi makro ekonomi Indonesia sudah mulai membaik. "Tapi incoming beat-nya untuk yang 11 tahun besar, yaitu Rp 8,6 triliun. Artinya, investor masih percaya sama republik ini," kata Chatib.

Secara terperinci, lima surat utang yang dilelang adalah seri SPN03131211 dengan yield tertinggi dimenangkan 5,8 persen, yang akan jatuh tempo pada 11 Desember 2013. Adapun jumlah nominal yang dimenangkan Rp 1 triliun dan nominal nonkompetitif yang dimenangkan Rp 1 triliun dengan bid-to-cover-ratio 7,84.

Sementara seri SPN12140911 dengan yield tertinggi dimenangkan 6,95 persen yang jatuh tempo pada 11 September 2014. Jumlah nominal yang dimenangkan Rp 2 triliun, nominal kompetitif yang dimenangkan Rp 1 triliun, dan nominal nonkompetitif yang dimenangkan Rp 1 triliun.

Sedangkan untuk seri FR0070, yield tertinggi yang dimenangkan 8,85 persen dengan tingkat kupon 8,375 persen, yang jatuh tempo 15 Maret 2024. Jumlah nominal yang dimenangkan Rp 3,35 triliun, nominal kompetitif yang dimenangkan Rp 2,85 triliun, dan nominal nonkompetitif yang dimenangkan Rp 500 miliar dengan bid-to-cover ratio 2,58.

Untuk seri FR0071, yield tertinggi dimenangkan 9,3 persen dengan tingkat kupon 9 persen dan akan jatuh tempo pada 15 Maret 2029. Adapun jumlah nominal yang dimenangkan Rp 2,4 triliun dengan nominal kompetitif yang dimenangkan Rp 2,075 triliun dan nominal nonkompetitif yang dimenangkan Rp 325 miliar. Adapun bid-to-cover ratio 1,62.

Sementara untuk seri FR0068, yield tertinggi yang dimenangkan 9,43 persen dengan tingkat kupon 8,375 persen, yang akan jatuh tempo pada 15 Maret 2034. Jumlah nominal yang dimenangkan adalah Rp 3,250 triliun dengan nominal kompetitif yang dimenangkan Rp 2,875 triliun dan nominal nonkompetitif yang dimenangkan Rp 375 miliar. Bid-to-cover ratio 1,53.

ANGGA SUKMA WIJAYA

Lelang SUN kebanjiran peminat

Oleh Dina Farisah - Rabu, 11 September 2013 | 06:34 WIB

JAKARTA. Lewat Direktorat Jenderal Pengelolaan Utang (DJPU), pemerintah kemarin menggelar lelang surat utang negara (SUN). Dari target indikatif yang ditetapkan Rp 8 triliun, total penawaran yang masuk mencapai Rp 32,644 triliun. Cuma, total lelang yang dimenangkan oleh pemerintah sebesar Rp 12 triliun.

Dari lima seri SUN yang ditawarkan, dua seri tenor pendek menjadi incaran investor. Seri SPN03131211 dengan total penawaran Rp 7,83 triliun dimenangkan Rp 1 triliun dengan yield tertimbang 5,54%. Lalu, seri SPN12140911 dengan total penawaran Rp 7,3 triliun dimenangkan Rp 2 triliun dengan yield tertimbang 6,93%.

Pemerintah lebih banyak memenangkan seri panjang. Seri FR0070, misalnya, dimenangkan Rp 3,35 triliun dengan yield tertimbang 8,79%. Seri FR0068 dimenangkan Rp 3,25 triliun dengan yield tertimbang 9,34%.

Head of Debt Research PT Danareksa Sekuritas, Yudistira Slamet menilai, antusiasme investor merefleksikan sentimen positif sudah masuk ke Indonesia. Volatilitas rupiah cenderung mereda beberapa hari terakhir. Harga obligasi juga sudah pada level terendah sehingga menjadi momentum masuk bagi investor.

Ekonom Bank Internasional Indonesia Josua Pardede bilang, dari sasaran pemilihan seri tenor pendek, ini mengindikasikan masih ada kekhawatiran dalam jangka panjang. Investor masih mewaspadai tapering off stimulus moneter dari The Fed. "Jika ada pemangkasan, yield SUN bisa naik lagi," kata dia.

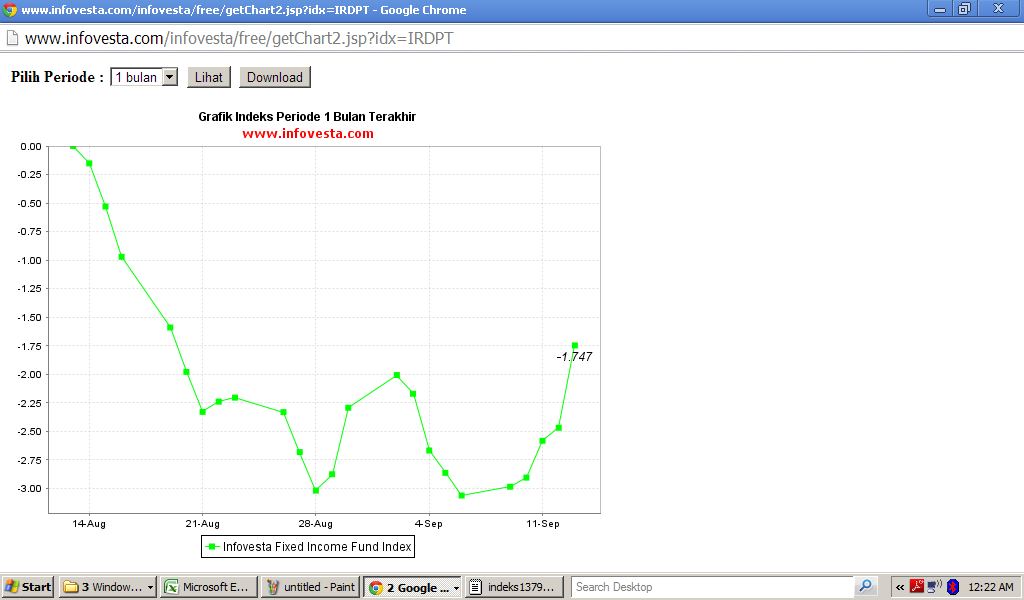

Sinyal siaga! Harga obligasi semakin jatuh

Oleh Wahyu Satriani - Selasa, 10 September 2013 | 06:30 WIB

kontan

JAKARTA. Sinyal kuning menyala dari pasar obligasi Indonesia. Tekanan hebat di pasar obligasi akibat kondisi ekonomi Indonesia yang memburuk membuat harga obligasi semakin terbenam.

Tengok saja, indeks harga surat utang negara (SUN), Senin (9/9), menyentuh level terendahnya sejak 2009 di posisi 94,26. Indeks ini turun 0,19% dari posisi Jumat (6/9) yang berada di 94,44.

Sejumlah SUN acuan alias benchmark juga mencatatkan koreksi terdalam. Salah satunya, harga SUN seri FR0065 bertenor 20 tahun, kemarin, turun ke level terendah sejak terbit tahun lalu di level 76,12. Otomatis, yield surat utang ini naik dari 9,20% di akhir pekan lalu menjadi 9,28%.

Jika dihitung sejak akhir 2012, ketika indeks harga SUN masih sebesar 111,70, return yang diperoleh investor obligasi negara dari capital gain harga SUN hingga kemarin, tercatat minus 15,61%.

Padahal, di tahun lalu, pasar obligasi masih mampu memberikan return kepada investor sekitar 12%. Di 2011 dan 2010, surat utang negara memberikan return masing-masing sebesar 22%.

Lonjakan inflasi sebagai buntut kenaikan harga bahan bakar minyak (BBM) bersubsidi yang diikuti oleh kenaikan suku bunga acuan Bank Indonesia (BI rate) menjadi biang kerok atas terjadinya koreksi tajam di pasar obligasi.

Namun, laju inflasi menjadi faktor penggerus paling menonjol karena obligasi ditransaksikan dengan kupon bunga tetap atau fixed rate. Asal tahu saja, hingga Agustus 2013 lalu, inflasi tahunan Indonesia sudah mencapai 8,79%.

"Jika inflasi naik, maka investor menginginkan yield lebih tinggi. Padahal kalau yield naik, harga obligasi akan turun," jelas Head of Fixed Income Research PT Mandiri Sekuritas Handy Yuniato.

Di lain sisi, meskipun pemerintah telah menaikkan harga BBM bersubsidi, namun defisit anggaran pemerintah tetap membengkak. Akibatnya, suplai surat utang semakin besar untuk menambal defisit anggaran. Ketika suplai surat utang bertambah, imbal hasil SUN mengalami kenaikan dan harga menjadi tertekan.

Tekanan di pasar obligasi semakin menjadi, setelah nilai tukar rupiah melemah terhadap dollar Amerika Serikat (AS) akibat defisit transaksi berjalan yang terus melebar. "Karena pemegang SUN saat ini sekitar 30% merupakan investor asing, sehingga pelemahan rupiah akan memicu outflow," tutur Handy. Terlebih, pada saat bersamaan, yield obligasi Amerika Serikat (US treasury) naik.

Korporasi pun juga ikut terkena getah akibat pasar obligasi yang melesu. Perusahaan harus mengeluarkan ongkos mahal untuk mendapatkan pendanaan dari obligasi. Dus, penerbitan obligasi korporasi di tahun ini tak bakal sebesar tahun lalu. Hingga kini, total penerbitan obligasi korporasi baru mencapai Rp 43,6 triliun dibandingkan sepanjang 2012 yang sekitar Rp 69,3 triliun.

"Diperkirakan pasokan obligasi baru korporasi di sisa tahun ini hanya sebesar Rp 11,1 triliun," ujar Vonny Widjaja, Direktur Pemeringkatan PT Pemeringkat Efek Indonesia (Pefindo).

Bukan cuma itu, beban pembayaran utang pemerintah membengkak, karena investor meminta imbal hasil tinggi setiap SUN terbit.

time2buy maseh neh pada akhir Juni 2013:

bandingkan dengan tren indeks reksa dana saham (3 taon):

iiiiiiiiiiiiiiiiJJJJJJJJJJJJJJJiiiiiiiiiiiiiiiiiiiiiiiii

Dalam 5 hari, asing tarik Rp 2,89 triliun dari SUN

Oleh Asnil Bambani Amri - Selasa, 11 Juni 2013 | 10:30 WIB

JAKARTA. Dalam waktu lima hari saja,

investor asing telah menjual kepemilikannya di pasar obligasi sebesar Rp

2,89 triliun. Mengutip data dari Direktorat Jenderal Pengelolaan Utang,

Kementerian Keuangan, posisi kepemilikan SUN oleh asing turun dari Rp

302,94 triliun (31/5), menjadi Rp 300,05 triliun (5/6).

Padahal nilai total SBN pada periode tersebut naik dari Rp 895,77

triliun menjadi Rp 898,87 triliun. kenaikan SBN ini terjadi karena

pemerintah menerbitkan SBN baru. Institusi yang banyak menyerap lelang

SBN terakhir adalah, perbankan dari Rp 306,26 triliun menjadi Rp 310,23

triliun.

bwat ANONIM yang tanya perbandingan SDP, schroder dana prestasi plus, n PDM:

keterangan: Schroder Dana Prestasi masuk kategori reksa dana campuran, Schroder Dana Prestasi Plus masuk RD Saham, dan PDM masuk RD saham.